Feature Story - PCI's Cost-Shifting Myth

Property Casualty Insurers Association of America ("PCI") has engaged in a year-long, anti-competitive campaign that - regrettably - has shown little regard for the facts, applicable law or actual data on performance of alternatives to traditional workers' compensation. Case in point, their June 6, 2016 report on "Cost Shifting from Workers' Comp Opt-Out Systems: Lessons from Texas and Oklahoma."

The obvious, material misstatements and exaggerations combined with a lack of actual Option program data, bring into question the need to even respond to this June 6th report.

If you need to know more:

1. The PCI cost shifting report boasts of using "verifiable and relevant data" and speaks to "the behavior of opt-out employers", but-in-fact-

a. fails to include any actual Texas or Oklahoma Option claims data. There is no evidence that PCI has even attempted to obtain such claims data, and

b. mischaracterizes the numbers, relying on inapplicable workers' compensation data from the National Council on Compensation Insurance.

2. The PCI report ignores the fact that actual Option program data suggests better medical outcomes - such as shorter disability durations and improved initial and sustained return to work.

3. The PCI report ignores the fact that Option programs pay better wage replacement benefits in most cases, which will be further demonstrated.

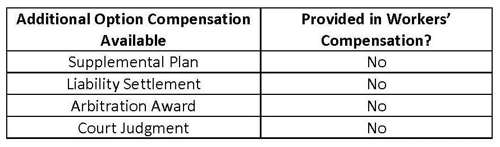

4. PCI fails to consider all benefit plan payments, supplemental plan payments, and negligence liability settlements and awards under Texas Option programs that are not available under workers' compensation.

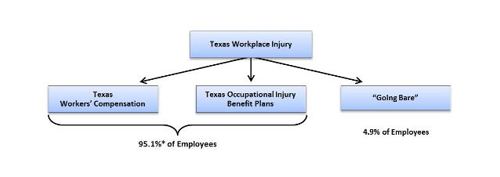

5. PCI fails to acknowledge the Texas Department of Insurance has determined that over 95% of Texas workers' are covered by either workers' compensation or an injury benefit plan.

6. PCI ignores the fact that workers' compensation systems completely exclude entire classes of workers from coverage. Perhaps before attacking responsible Texas and Oklahoma employers who actually provide injury benefit coverage for their workers, PCI should first focus its attention on the approximately 14 million American workers across all states that have no on-the-job injury benefits coverage whatsoever.

7. PCI makes false statements regarding Oklahoma Option medical benefit duration limits that the law does not permit and are not found in any qualified Oklahoma Option plan.

8. PCI criticizes Oklahoma Option benefit limitations that are verbatim from the Oklahoma workers' compensation law.

9. PCI further extrapolates its false model to Tennessee and south Carolina despite the fact that Option programs proposed in those states - unlike Texas - have mandated benefits. No bill has been introduced in either of those states to allow employers to "go bare."

10. PCI fails to acknowledge Option program compliance with Medicare reporting and MSA requirements. The Centers for Medicare and Medicaid Services has stated that Texas Option programs are subject to liability coverage rules. Option programs normally pay full benefits before medicare pays anything. Texas Option programs also routinely comply with Medicare quarterly, electronic reporting rules on open medical claims and liability settlements involving injured employees that are medicare beneficiaries. CMS can (and does) seek reimbursement from Option programs. Texas Option programs also protect Medicare's primary interest before settling claims with Medicare beneficiaries by determining any amounts owed to CMS for medical payments, assessing potential future medical payments that the injured employee may have, and then setting aside a portion of the settlement funds to pay for future treatment.

11. PCI's analysis further implodes when making the claim that every dollar saved by an employer equals a dollar of cost shifting to taxpayers. This fatalistic viewpoint suggests that workers' compensation systems simply cannot be improved. A simple Google search of "workers' comp fraud you tube" suggests otherwise. Moreover, group health plans typically provide more efficient care at a lower cost than workers' compensation. Using an ERISA-based plan to optimize delivery of medical care at a lower cost does not mean that those cost savings result in cost shifting.

12. PCI's analysis relies heavily on the fact that Option programs include certain limitations and exclusions on coverage:

a. ignoring the fact that workers' compensation systems also include various limitations and exclusions on coverage (including dollar and duration caps), and

b. erroneously suggesting that such limitations and exclusions come into play at every turn and opportunity. They simply don't. Consider the legal duty (and personal liability exposure) under ERISA for fiduciaries to administer claims in the best interests of injured workers. Further, see PartnerSource's recommendations for benefit coverage enhancements.

13. PCI surely realizes these same (and far bigger) concerns about cost-shifting fro workers' compensation are being used to support a federal government takeover of workers' compensation. For example, Professor John Burton has proposed federal workers' compensation standards, which would seem to be unpopular with the same commercial insurance companies PCI represents.

14. This cost shifting report and unbridled criticism from PCI (claiming its research "is relevant for all states") is surprising in view of the PCI board's approval in July 2015 of criteria for an acceptable alternative to workers' compensation, which was finally unveiled to the public at the Workers' Compensation Research Institute conference on March 10, 2016.

15. PCI's assumption of cost shifting is an attempt to divert attention from the benefits of the Option and avoid competition. PCI's over-playing of the cost shifting card is also obvious to workers' compensation thought leaders. For example, David DePaolo notes (among other things) in his column, "The REAL Objection to Opt Out" that, "Each statistic cited by PCI against opt out can be asserted against traditional work comp - just use another study or data source."

Misinformation like this PCI report only serves to further limit workers' compensation system innovation. By working together, we can improve both traditional workers' compensation and competitive alternatives for employers and injured employees alike. Isn't that the objective the entire industry should be working toward?